The FDIC’s $250,000 Limit: What It Means for Bank Depositors

The Federal Deposit Insurance Corporation (FDIC) provides insurance coverage for deposit accounts in participating banks, ensuring that depositors’ funds are protected up to a certain limit in the event of a bank failure. But what exactly does this mean, and how much is covered?

What is FDIC Insurance?

FDIC insurance is designed to promote confidence in the banking system by insuring deposits in participating banks. Since its establishment in 1933, the FDIC has provided a safety net for depositors, ensuring that their funds are protected up to the insured limit. This insurance coverage applies to a wide range of deposit products, including:

- Checking Accounts: Everyday accounts used for managing finances

- Savings Accounts: Accounts for saving money over time

- Money Market Deposit Accounts: Accounts that earn interest and offer limited check-writing privileges

- Certificates of Deposit (CDs): Time deposits with fixed interest rates and maturity dates

- Cashier’s Checks and Money Orders: Official payment instruments issued by banks

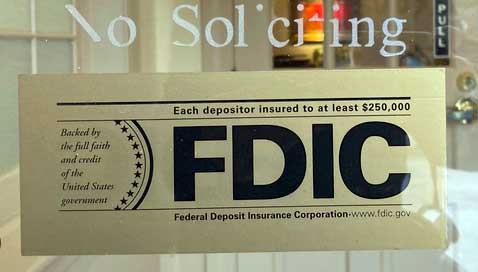

FDIC-Insured Limit

The standard deposit insurance coverage limit is $250,000 per depositor, per FDIC-insured bank, per ownership category. This means that if you have multiple accounts in the same ownership category at the same bank, the total coverage limit is still $250,000. However, if you have accounts in different ownership categories or at different banks, you may be eligible for additional coverage.

Ownership Categories

The FDIC insures deposits based on ownership categories, which include ¹:

- Single Accounts: Accounts owned by one person, with a coverage limit of $250,000 per owner

- Joint Accounts: Accounts owned by two or more persons, with a coverage limit of $250,000 per co-owner

- Certain Retirement Accounts: Accounts like IRAs, with a coverage limit of $250,000 per owner

- Trust Accounts: Accounts with beneficiaries, which may have higher coverage limits depending on the number of beneficiaries

- Corporation, Partnership, and Unincorporated Association Accounts: Accounts for businesses, with a coverage limit of $250,000 per entity

How FDIC Insurance Works

If your bank fails, the FDIC will typically resolve the situation by selling the bank to another FDIC-insured institution or by paying depositors directly. In either case, the FDIC ensures that depositors have access to their insured funds as quickly as possible. Since the FDIC’s inception, no depositor has lost a single penny of insured deposits.

Verifying FDIC Insurance

To confirm whether your bank is FDIC-insured, you can use the BankFind tool on the FDIC’s website or call the FDIC at 1-877-ASK-FDIC (1-877-275-3342). You can also check for the FDIC logo at your bank’s branch or on its website.

By understanding FDIC insurance and its coverage limits, you can ensure that your deposits are protected and make informed decisions about your financial security ¹.